CoinDeskAug 02, 06:50 AM

Strategy Keeps STRC Dividend at 12%

Strategy said it is holding the dividend on its STRC preferred stock at 12%. The decision keeps the payout unchanged for investors in the company’s yield-focused security.

ReadIllinois has approved a crypto transaction tax, drawing criticism from industry advocates who say it has no clear parallel in traditional state financial markets. a16z general counsel Miles Jennings argued that comparable state taxes on stocks, bonds or derivatives effectively do not exist in the US.

Illinois has approved a crypto transaction tax, drawing criticism from industry advocates who say it has no clear parallel in traditional state financial markets. a16z general counsel Miles Jennings argued that comparable state taxes on stocks, bonds or derivatives effectively do not exist in the US.

The development matters because industry critics view the tax as setting crypto apart from other financial markets at the state level. a16z general counsel Miles Jennings said there is “effectively no comparable state financial transaction tax” on stocks, bonds or derivatives anywhere in the country.

Illinois Governor J.B. Pritzker has approved a crypto transaction tax despite pushback from crypto advocates and industry executives, according to Cointelegraph. The measure has prompted criticism from legal and policy voices in the digital asset sector.

The development matters because industry critics view the tax as setting crypto apart from other financial markets at the state level. a16z general counsel Miles Jennings said there is “effectively no comparable state financial transaction tax” on stocks, bonds or derivatives anywhere in the country.

That comparison is central to the backlash. Crypto companies and advocates have long argued that digital asset businesses should not face rules that are more burdensome than those applied to traditional financial activity, unless lawmakers clearly justify the distinction.

The Illinois move adds to the broader US policy debate over how states should regulate and tax crypto transactions. For companies operating in the sector, state-level tax policy can affect compliance planning and decisions about where to serve customers.

The source material did not specify the tax rate, implementation timeline or which transaction types are covered. Those details will be important for market participants assessing the practical impact of the new Illinois policy.

Keep exploring

Strategy said it is holding the dividend on its STRC preferred stock at 12%. The decision keeps the payout unchanged for investors in the company’s yield-focused security.

Read

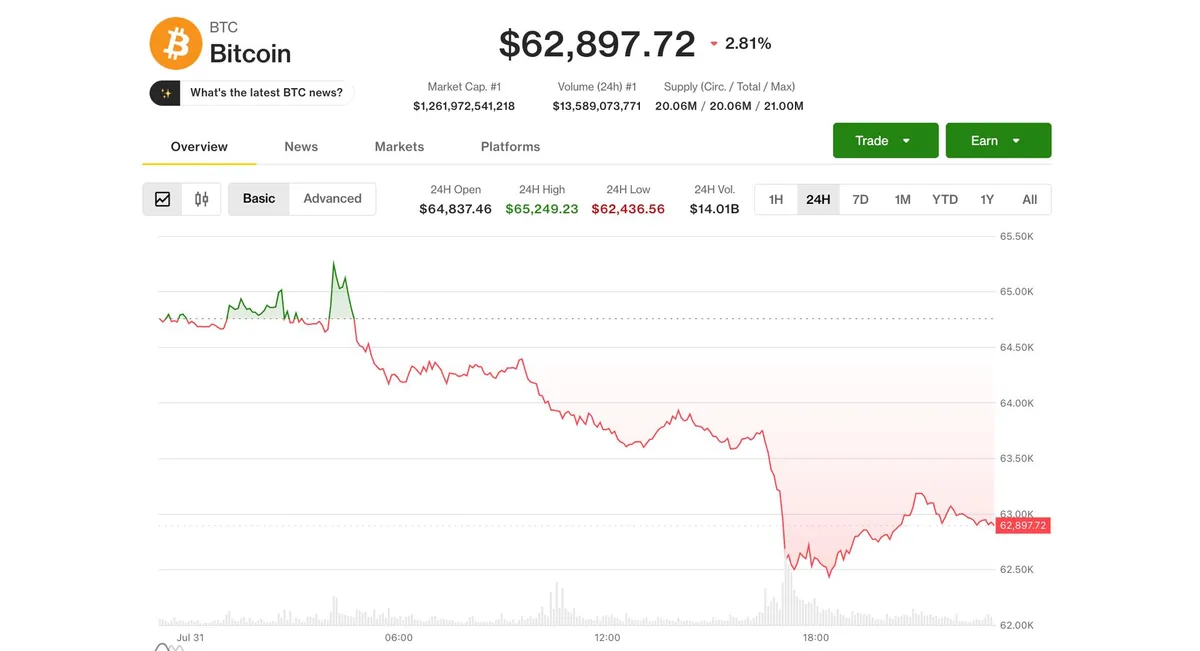

Bitcoin ended July with a monthly gain, though analysts expect August could be more volatile. They said the recent forced-selling pressure that weighed on the market appears to have already run its course.

Read

The latest State of Crypto update says the industry has two weeks left in the push for the Clarity effort. The development keeps attention on U.S. crypto policy as companies and market participants watch for regulatory direction.

Read